Europe’s power markets have once again entered a phase of heightened volatility. A key trigger has been the recent geopolitical disruption linked to tensions around the Strait of Hormuz. Within one month of the conflict, EU natural gas prices surged by approximately 70%, while oil prices increased by 60%, according to EU energy officials. The impact on electricity markets has been immediate, particularly in countries with high gas dependency.

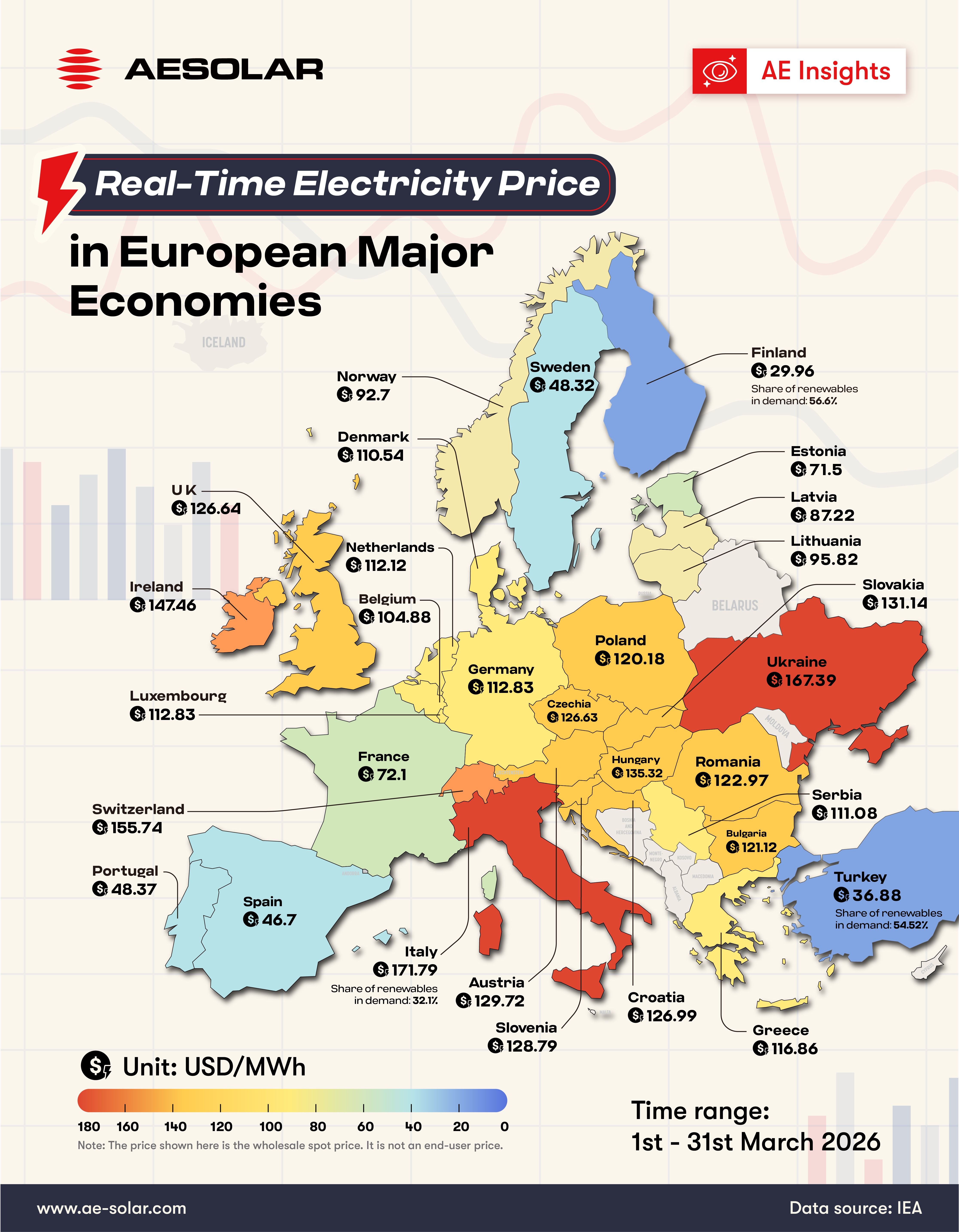

Take Greece as a representative case: with 45.42% of electricity generation linked to natural gas, its wholesale power price rose from 97.92 USD/MWh in February to 116.86 USD/MWh in March, an increase of over 19%. In Latvia, where gas accounts for 69.22% of the generation mix, price volatility has been even more pronounced.

In contrast, markets with higher renewable penetration demonstrated greater resilience. Southern Europe offers a clear example—Spain (46.7 USD/MWh) and Portugal (48.37 USD/MWh) recorded some of the lowest electricity prices in Europe during the same period. This was supported by strong solar generation, with both countries setting new solar output records in March, effectively suppressing daytime prices.

These dynamics reinforce a critical conclusion: electricity price stability in Europe is increasingly tied to renewable energy deployment, particularly solar.

The Strategic Role of the Clean Industrial Deal

This market behavior aligns closely with the strategic direction set by the EU Clean Industrial Deal, introduced in early 2025. While often framed as an industrial competitiveness initiative, its implications for energy independence are equally significant.

The policy aims to reduce Europe’s exposure to imported fossil fuels by accelerating electrification and scaling domestic clean energy capacity. In practice, this means:

- Expanding renewable generation, especially solar and wind

- Strengthening grid infrastructure and flexibility

- Supporting industrial decarbonisation through electrification

Despite being introduced over a year ago, the recent price shocks underline its continued relevance. Europe has now experienced three major energy shocks in four years, each reinforcing the same structural vulnerability: reliance on external fossil fuel supply chains.

Outlook: Renewables as a Hedge Against Volatility

From an investment and system design perspective, the implications are clear. Markets with higher shares of renewables—particularly those exceeding 50% in electricity demand, such as Finland (56.6%) and Turkey (54.52%)—are demonstrating lower price levels and reduced exposure to external shocks.

At the same time, rising electricity demand driven by electrification, data centers, and industrial recovery is expected to continue. This creates a dual pressure:

More power is needed

It must be more stable and locally sourced

Solar PV, due to its scalability, declining LCOE, and rapid deployment cycle, is uniquely positioned to address both.

Europe is transitioning from a fossil-fuel-driven pricing model toward a system increasingly shaped by renewable generation profiles and grid integration capacity. For developers, investors, and industrial consumers, this shift presents both risk and opportunity. The ability to secure stable, low-cost electricity will increasingly depend on access to renewable assets and integrated energy solutions.